Banks to face up to a stark choice

Jeff Sea and Steve Punch say local banks have an opportunity to use the Foreign Account Tax Compliance Act (FATCA) to their advantage.

Jeff Sea and Steve Punch say local banks have an opportunity to use the Foreign Account Tax Compliance Act (FATCA) to their advantage.

Banks and other financial institutions (FIs) across the world are now preparing for the imminent implementation of FATCA regulations.

Some have said that FATCA is “an atomic bomb burden”, while others believe it may be an opportunity for them to show their transparency, competitiveness and strong corporate governance focus by complying with FATCA.

FATCA was enacted in 2010 to prevent and detect offshore tax evasion by US taxpayers. To do so, FATCA sets out a comprehensive and complex set of rules which will impact almost every financial institution around the world. Banks, funds and other institutions failing to comply with FATCA could effectively be forced out of US financial markets, or investing in US assets. The crackdown on overseas tax evasion by US “persons” is fast changing shape as officials move to implement it via country-to-country agreements, rather than by enforcing a single law for all financial institutions.

How does FATCA impact FIs in Vietnam?

With the enactment of FATCA, foreign financial institutions (FFIs) generally must conduct due diligence on their account holders and investors to determine whether their accounts are “US accounts”. Additionally, FFIs will face a choice of whether they will sign an FFI agreement and agreed to identify and report to the US tax authority, the Internal Revenue Service (IRS), information about direct and indirect US account holders, or be subject to 30 per cent withholding tax on all direct or indirect US source income.

It should be noted that FATCA is not designed as a tax collection by the IRS, but more toward forcing FFI around the world to report its US accounts holders. Thus the implications on banking processes in extracting required information for IRS reporting and identifying existing US accounts holders, knowing on-boarding new customers are enormous. So too are the annual reporting requirements a compliant FFI’s will need to provide to the IRS. The question now is whether any Vietnamese bank is ready for this or be excluded from US financial market?

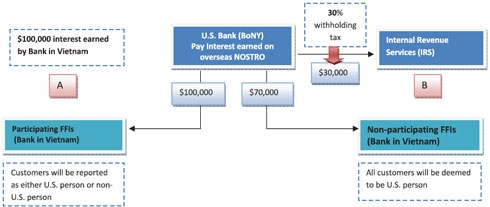

Illustrative example of how FATCA works

A Bank in Vietnam (i.e. an FFI) has overseas NOSTRO account in Bank of New York which earns USD100,000 interest monthly. A) If the FFI is a Participating FFI (PFFI), Bank of New York will withhold 0% of interest payable to the Bank in Vietnam. B) If the FFI is a Non-participating FFI (NPFFI), Bank of New York will withhold 30% of interest payable to the Bank in Vietnam

Model of intergovernmental agreements

After first releasing its draft FATCA regulation in February 2012, the IRS has attempted to ease the burden of FATCA compliance for FI’s by introducing the draft model Intergovernmental Agreement (IGA) on July 26, 2012.

There are two versions of the model IGA — a reciprocal version and a nonreciprocal version. The former allows FFIs report to a local government agency first and then to the US IRS, while the latter allows FIs report directly to IRS. This respects potential local privacy laws in overseas countries. When an IGA is signed, the FIs in that participating country will then be governed by the local legislation, therefore local domestic legislation will be likely required.

The “big guys”, UK, France, Italy, Spain, and Germany, have agreed to the FATCA-principle and are entering into agreement with the US as seeing that FATCA is a new opportunity. On September 14, 2012, the UK and the US officially signed bilateral reciprocal IGA. The UK plans to commence apply the new FATCA legislation in early 2013.

US Treasury is now negotiating with at least 40 countries for FATCA tax information-sharing pacts. The OCED recently stated that it welcomed the cooperation between the US and the pioneer countries. In fact, OCED has expressed its intent to work closely with interested countries and stakeholders to design a common model for automatic exchange of information. This includes the development of reporting and due diligence standards for financial institutions. In the Asia-Pacific region, Japan has commenced negotiations with the US on IGA and other developed countries (i.e. Australia, Hong Kong, Singapore and South Korea) are now considering entering an IGA with the US.

The IGA significantly benefits FIs by reducing reporting requirements and protecting the privacy of individuals. However, it only applies to countries which have US double tax agreements (DTA).

Vietnam and the US have not yet signed an DTA. However, US officials have indicated that non-DTA countries will soon be offered a similar arrangement as countries with which it has a DTA. As of today, the final details are not yet available. The suggestion for Vietnam is that the Vietnamese tax authority, General Department of Taxation (GDT) could seek to initiate dialogue with the US to resolve any potential conflict between FATCA and Vietnamese law. By announcing its intention on FATCA compliance, Vietnam could then sell itself as an attractive jurisdiction that is considered proactive, transparent, and competitive, whilst protecting the rights of all investors.

Early planning is required

Even though the IRS has extended the effective date to become a participating FFI until January 1, 2014, banks, fund managers and insurers around the world have already commenced FATCA projects designed to become compliant and sign an FFI agreement prior to the IRS deadline in December, 2013.

FATCA compliant FIs may be able to achieve a competitive advantage through enhanced customer relationship and capital-raising capabilities. Prudent banks and other FIs will allow themselves sufficient time to develop business requirements and IT capabilities to comply with FATCA. A recent KPMG survey, “FATCA Readiness of Financial Institutions” highlighted that 25 per cent of FI’s had commenced their FATCA compliance programmes.

A further 25 per cent of respondents think that they will not be able to comply with the deadline and 36 per cent reported that they are uncertain whether they can meet the deadline even in the light of potential commercial and reputational risk for non-compliance.

No doubt that FATCA is a challenge for FIs, 54 per cent of respondents agree with this point.

Moreover, the respondents say that the most challenging aspect of FATCA compliance is the actual reporting and documentation requirements, rather than the customer account identification and withholding scheme.

Already many of the foreign banks and foreign bank branches in Vietnam have commenced their global FATCA projects. While their task is much larger, the process and requirements are the same. Irrespective of when or whether the Vietnamese authority makes comment on FATCA, local FI’s will be affected from January 1, 2014. This means that FIs in Vietnam should conduct a preliminary assessment of their ability to comply with the FATCA framework and to evaluate necessary modifications to the existing processes and systems. Vietnamese banks and other local financial institutions should act now.n

For more information, please contact: (*) Jeff Sea – tax partner, KPMG in Vietnam at jeffsea@kpmg.com.vn and Steve Punch – Risk & Consulting director, KPMG in Vietnam at spunch@kpmg.com.vn. The views expressed by the authors here do not necessarily represent the views and opinions of KPMG.

What the stars mean:

★ Poor ★ ★ Promising ★★★ Good ★★★★ Very good ★★★★★ Exceptional

Tag:

Tag:Related Contents

Latest News

More News

- KPMG launches tariff modeller in Vietnam to navigate US tariff risks (July 29, 2025 | 12:11)

- Removing hidden barriers to unlock ASEAN trade (June 29, 2025 | 11:31)

- New report charts path for Vietnam’s clinical trial growth (May 21, 2025 | 08:58)

- TTC Agris strengthens market position with investment in Bien Hoa Consumer JSC (May 19, 2025 | 10:14)

- World Bank to help SBV build shared database for banking industry (April 09, 2025 | 08:55)

- New trade alliances and investment hubs are redefining global power dynamics (April 03, 2025 | 17:00)

- ACCA and KPMG forge path for business leaders to pioneer ESG excellence (March 07, 2025 | 10:09)

- VietBank signs MoU with KPMG (February 26, 2025 | 18:47)

- Warrick Cleine MBE: an honour for services to British trade and investment in Vietnam (December 31, 2024 | 20:16)

- KPMG report offers fresh insight into leveraging AI (December 24, 2024 | 09:23)

Mobile Version

Mobile Version