Auto firms to face tax hit

According to Vietnam Automobile Manufacturers Association (VAMA), to benefit from preferential tariffs under the ASEAN Trade in Goods Agreement (ATIGA) when opening customs declarations, VAMA member companies as importers showed out their certificates of origin (C/O) form D and relevant customs records as per existing regulations, which were approved by customs bodies.

According to Vietnam Automobile Manufacturers Association (VAMA), to benefit from preferential tariffs under the ASEAN Trade in Goods Agreement (ATIGA) when opening customs declarations, VAMA member companies as importers showed out their certificates of origin (C/O) form D and relevant customs records as per existing regulations, which were approved by customs bodies.

This means they were eligible to enjoy special import tariff rates from zero to 5 per cent.

C/O form D are honoured on goods having from 40 per cent production value made in the ASEAN region.

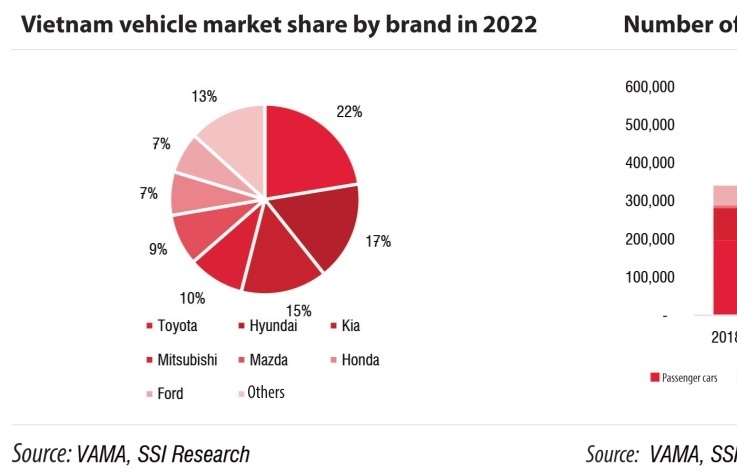

However, relevant competent agencies are reportedly reviewing import records of auto joint ventures relevant to C/O form D and associated bills of lading. They are even considering collecting tax differences worth trillions of dong arguing that with presented papers, several auto joint ventures came below par to benefit from ATIGA tax preferences. Affected auto firms included Toyota, Ford, Mitsubishi and several others.

Dispatch 554/GSQL dated August 17, 2012 of the General Department of Customs stipulates ‘Importers wanted to enjoy tax preferences ought to submit to customs bodies in the importing country at the time of making customs declarations through bill of lading granted in the territory of exporting country.’

VAMA, however, assumed the proposal did not match what was said in the Ministry of Industry and Trade’s (MoIT) Circular 21/2010/TT-BCT, Appendix 7, Clause 13 dated May 17, 2010 referring to implementation of C/O principle in ATIGA.

Accordingly, to enjoy tax preferences at the time of making import procedures importers must submit to customs bodies in the importing country import declarations, C/O and proving documents and other documents pursuant to legal documents of member import country.

In its recent proposal sent to the government and competent agencies, VAMA argued since VAMA members/importers used the mode of directly transporting goods from exporting countries to Vietnam not making transit in third country they shall be required to submit common bill of lading only but not that granted by exporting countries.

Also according to VAMA, in ocean shipping besides the common bill of lading, there are special bills of lading in case of making transit in third country and having the participation of above two shipping firms. In this case, through bill of lading granted in exporting country is to showcase the products being transported directly from exporting to importing country. That is why under MoIT’s Circular 21 through bill of lading is only requested when necessary but not apply to all shipments.

A VAMA expert said: “Global auto groups are handling operations in the direction of their regional offices carrying out trade activities and issuing sale invoices to shipments whereas their factories based in different countries conduct production under their group instructions. This means to deliver bill of lading granted in export country, they will have to scale up expenses to place people in each exporting country just to meet Vietnam conditions. Meanwhile by essence this is only a common bill of lading but not through bill of lading with transit in third country as though by Vietnamese competent agencies.”

Auto firms reportedly met with the MoIT to make clear the spirit of C/O principle in ATIGA to source proper instructions relevant to preferential import tariff calculation towards auto joint ventures.

What the stars mean:

★ Poor ★ ★ Promising ★★★ Good ★★★★ Very good ★★★★★ Exceptional

Tag:

Tag:Related Contents

Latest News

More News

- Japan's Tokyu researches semiconductor technology in Binh Duong (April 15, 2024 | 07:12)

- Sunwah Group intensifies investment endeavours (April 12, 2024 | 19:12)

- China's BYD sets eyes on Vietnam (April 12, 2024 | 17:25)

- Shanghai to boost trade with Vietnam (April 12, 2024 | 17:23)

- EU ambassadors study investment climate in Da Nang city (April 11, 2024 | 17:17)

- Vietnam ready to ride US investment wave (April 11, 2024 | 17:11)

- Component makers display intent to establish networks (April 11, 2024 | 09:46)

- Foreign investors target smarter production chain (April 11, 2024 | 09:43)

- Vietnam to overhaul Law on Science and Technology (April 11, 2024 | 08:00)

- US company steps up AI investment in Southeast Asia (April 10, 2024 | 16:32)

Mobile Version

Mobile Version